Inflation jumped unexpectedly to 3.6pc in June, up from 3.4pc in May, despite hopes price growth would slow.

Transport, particularly the cost of petrol, made the largest upward contribution to the increase, according to the Office for National Statistics (ONS). Food and beverage costs also rose.

Core inflation, which strips out volatile prices from food and energy costs, measured 3.7pc, up from 3.5pc the previous month, while services inflation slowed to 5.2pc. In response to the figure, Chancellor Rachel Reeves said she knew that “working people” were still struggling with the cost of living, and while the Government has taken steps to help alleviate pressures “there is more to do”.

News of the surprise increase could mean we’re less likely to see multiple Bank of England rate cuts this year as inflation is still well above the central bank’s 2pc target. The Bank of England held interest rates to 4.25pc in June, but economists still expect it to cut its headline rate at the next decision on August 7.

Governor Andrew Bailey had also indicated that policymakers might look past inflation data, saying they would lower borrowing costs if they begin to see signs of weakness in the jobs market.

This could have a significant impact on your finances – including savings, mortgages and investments. Here, Telegraph Money explains what your options are:

-

What does the latest inflation figure mean for your mortgage?

-

What does rising inflation mean for your savings?

-

What does it mean for your pensions and investments?

What is inflation?

Inflation is the term used by economists and governments to describe the speed at which prices are rising.

In Britain, we usually measure inflation by comparing the price of a particular item to its price at the same time the previous year.

For example, if a chocolate bar cost £1 in May 2024 and then in May 2025 it costs £1.04, its price has risen by 4pc and thus inflation for this particular item stands at 4pc.

However, statisticians have to calculate the pace of price rises across the whole of the economy and use a variety of methods to estimate this as accurately as possible.

The most closely followed of these methods used by the Government and the Bank of England (BoE) is the Consumer Price Index, often abbreviated to CPI, which is published each month by the Office for National Statistics (ONS).

This calculates inflation based on a basket of hundreds of goods and services, which statisticians at the ONS update every year.

What does the latest inflation figure mean for your mortgage?

Higher inflation means we are less likely to see Bank Rate cuts, and therefore lenders will be less likely to cut mortgage rates – so borrowing may be more expensive.

Story ContinuesMortgage rates have remained high over the past two years, adding financial pressure across the housing market.

For first-time buyers, higher rates of borrowing have made it harder to get on the housing ladder, while existing homeowners face a mortgage shock when coming off ultra-low fixed rate deals and on to new loans at today’s rates.

At the time of writing, the average two-year fixed rate mortgage is 5.03pc, according to analyst Moneyfacts.

Fixed-rate and variable-rate mortgages are linked to the Bank Rate, although not necessarily directly.

Nathan Emerson, of trade body Propertymark, said: “This news will provide no respite for people who are struggling with their personal finances at a time when there is widespread data suggesting Britain’s finances are in a ‘perilous’ state.

“Housing plays a pivotal role in the UK economy, and considering the UK Government and the devolved administrations have set themselves ambitious housing targets, it’s important that there is strong affordability to support consumers with their housing ambitions.”

If you’re due to remortgage soon, our mortgage cost calculator can tell you how a new deal will affect your monthly bills.

What can you do if you need to get a mortgage?

For homeowners coming to the end of their fixed-rate mortgage it is important to remember you can start reviewing your options three to six months in advance and lock into a deal without committing to it. If rates then go up before you need to finalise your loan you are safe, but if rates fall in the interim you can choose a better deal.

Nicholas Mendes of broker John Charcol said: “For mortgage holders with less than six months remaining on their fixed-rate deal, it is advisable to start reviewing your options now.

“Many lenders allow you to lock in a new rate up to six months in advance, which could shield you from potential further increases.”

What are the best deals on the market?

For those purchasing a property, at the time of writing one of the best two-year fixed deals on the market is from Lloyds, at 3.69pc. You’ll need to have a deposit of at least 40pc, and it comes with a £999 fee. One of the cheapest five-year deals also comes from Lloyds, at 3.84pc and also with a £999 fee.

If you are remortgaging with 40pc equity, Lloyds 3.83pc deal is one of the cheapest, although it comes with a £999 product fee – as does its five-year deal, which comes in at 3.85pc.

What does rising inflation mean for your savings?

Rising inflation is bad news for savers, particularly when the Bank Rate is on the way down. While there are still some deals on the market that can beat the June rate of 3.6pc, you’ll need to make more of an effort to find them.

That being said, if the Bank of England slows future Rate cuts then savings rates may not fall quite as quickly as they could have done otherwise.

The average easy access savings rate is currently 2.67pc, according to Moneyfacts, but the most competitive accounts still pay around 5pc – though they are becoming increasingly rare.

Alice Haine, personal finance analyst at Bestinvest by Evelyn Partners said: “Savings rates have eased back dramatically following four rate reductions from the BoE since last summer, so the latest uptick in inflation is another blow for real returns.

“The bigger problem for savers is the post-tax net return on their cash holdings, something that is becoming increasingly problematic as more taxpayers get dragged into higher rates of tax as their incomes increase. This is a direct consequence of personal tax thresholds remaining stuck on pause until at least 2028, with those in higher tax bands likely to see their real returns net of tax only marginally positive on the most competitive accounts.”

“With savings rates likely to ease back even further in the months ahead, scouring the market for the best deals possible can help to extend that inflation-beating return, at least in the short-to-medium term.”

It’s important to make sure your savings are earning a rate higher than inflation wherever possible, as inflationary price rises eat into the value of savings – put simply, the rising prices mean your money won’t be able to buy as much as it previously could.

Our inflation calculator can show you how much your savings are being eroded by price increases.

What can you do about it?

As a minimum, you should check your current savings rates and make sure they’re higher than the inflation rate.

Planning ahead, it might be a good time to commit to a fixed-term account if there’s cash you won’t need to access for at least a year.

Derek Sprawling, managing director of Spring savings, said: “The increase in the rate of inflation further erodes the value of savings earning a poor rate of interest. With over a half a trillion pounds sitting generating nothing or 1.5pc or less, savers need to act and make their money work harder to maintain its value.

“Of course, everybody will have their own inflation rate based on individual circumstances and that is likely to be more than the official figure given the upwards cost pressure on housing, utilities, food and general living. The good news is that there are still options for people to generate a return above the rate of inflation and I would urge people to not accept a poor return on their cash.”

What’s the best deal on the market?

At the time of writing, Chase’s easy-access account is offering 5pc paid monthly.

For a fixed account, Oxbury pays 4.62pc for a six-month bond, with a minimum deposit of £1,000.

To find top savings rates, updated daily, see our guides to the best easy-access accounts and best fixed-rate bonds. You can also find the best notice accounts, top regular savers and best rates available for current accounts that pay interest.

For options to protect your returns from tax, see our guide to the best cash Isas and best lifetime Isas.

And, if you want to put money away for your children, see our guides to the best Junior Isas and best children’s savings accounts.

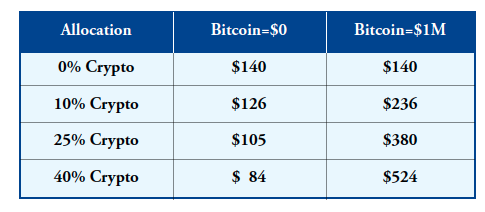

What does it mean for your pensions and investments?

The stock market is not officially linked to inflation or the Bank Rate, but as both are significant indicators of the state of the economy, they can have a big impact on investor sentiment.

With rising inflation eroding the value of cash savings, some may turn to investing in a bid to get higher returns.

Kevin Mountford, of bank Raisin UK, said: “The Bank of England has been clear that it’s watching not just inflation, but the broader state of the economy, to determine a rate cut in August. Slowing wage growth and signs that employers are reducing hours or headcount suggest the job market is softening, partly in response to higher business costs, such as the national insurance rise.

“However, the figures today suggest the Bank may hold its nerve a little longer. The balance could still be tipped, so for savers, time may be running out to lock in competitive fixed rates, especially on longer-term accounts.”

However, it’s important not to make any rash decisions based on inflation data alone. Investing should be for the long term, as Dean Butler, of Standard Life, part of Phoenix Group, explained: “For those able to accept a level of risk, investing offers the potential for higher growth, but remember that investments can go down as well as up. If you’re able to take a long-term view, pensions are a powerful tool, combining potential compound investment growth over many years with employer contributions and tax efficiency.”

For those planning their retirement, annuities can offer guaranteed retirement income when you’re no longer working. Some are inflation-linked, which can help with rising costs over time.

Broaden your horizons with award-winning British journalism. Try The Telegraph free for 1 month with unlimited access to our award-winning website, exclusive app, money-saving offers and more.